Australian industrial vacancy falls to a new record low - Knight Frank

Contact

Jun 7, 2023

Australian industrial vacancy falls to a new record low - Knight Frank

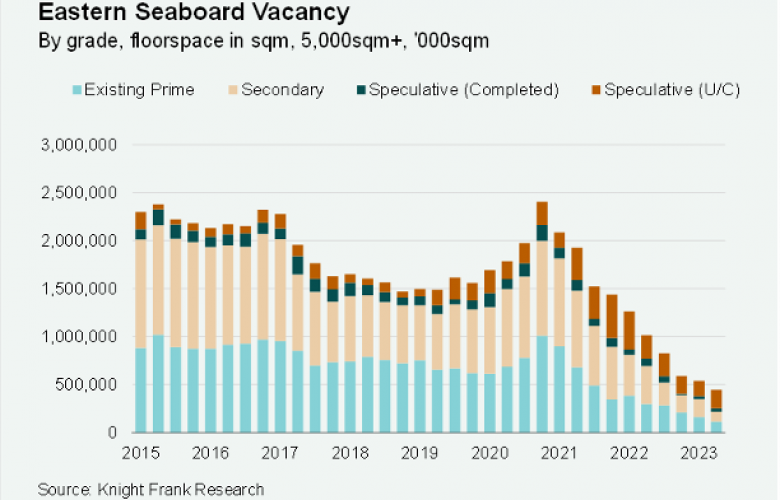

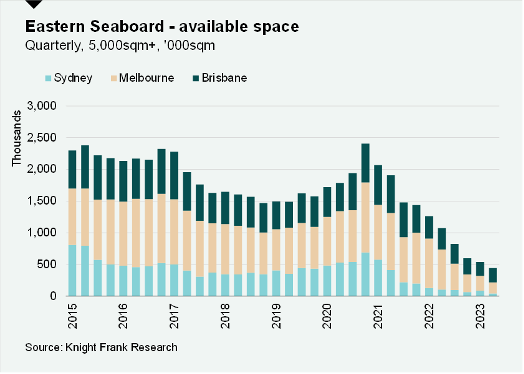

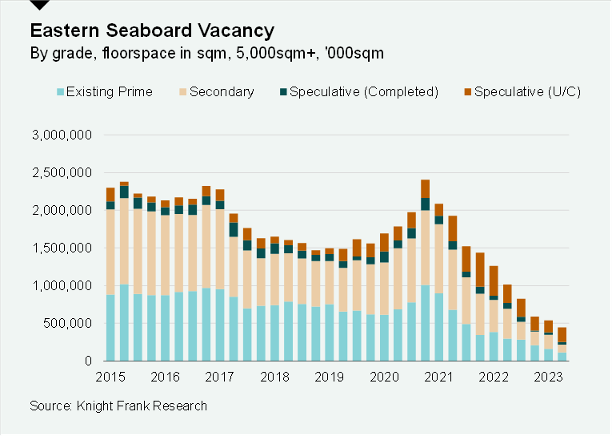

Industrial vacancy in the East Coast capital cities continues to fall to new lows, with only 444,681sq now available following an 18 per cent fall in available space over the first quarter of 2023, according to the latest research from Knight Frank.

-

Image supplied by Knight Frank.

Image supplied by Knight Frank. -

-

-

Industrial vacancy in the East Coast capital cities continues to fall to new lows, with only 444,681sq now available following an 18 per cent fall in available space over the first quarter of 2023, according to the latest research from Knight Frank.

Knight Frank’s Australian Industrial Review Q1 2023 found Sydney (43,759sq m) was the tightest market, recording a 51 per cent contraction, and the city, along with Melbourne (174,330sq m), reached new lows in available space.

Brisbane (226,592sq m) increased marginally with an influx of new speculative development starts.

51 per cent of the remaining available space across the Eastern Seaboard is now in Brisbane, with 39 per cent in Melbourne and just 10 per cent in Sydney.

The overall drop in vacancy across the Eastern Seaboard cities follows a 56 per cent fall over the 2022 calendar year, and an eight per cent fall over Q4 2022 to see vacancy sit at 547,748sq m.

Across Australia’s East Coast there is now almost 2 million square metres less space available now than was the case in the peak in October 2020, when there was 2,405,857sq m available, equating to an 82 per cent fall.

Knight Frank Partner, Research and Consulting Jennelle Wilson said take up over the first quarter of 2023 was impacted by the limited opportunities on the market, being 26 per cent below the three-year average, totalling 515,653.

“Intense competition among tenants for limited available space resulted in further rental growth across all the Eastern Seaboard capital cities,” she said.

“Brisbane led the quarterly rental growth by an 8.6 per cent increase, followed by Sydney at 8.2 per cent, with this city overtaking Perth for the fastest growing rents year on year, with prime rents up by 38 per cent over 12 months.

“Adelaide and Perth reported 2.5 per cent and two per cent rental growth over the same period, while Melbourne saw moderate growth of 1.5 per cent on limited deals across most submarkets.

“Incentives continued to decline in Q1 and currently average 10 per cent across the Eastern Seaboard, which stimulated stronger growth in effective rents over the quarter.”

According to Knight Frank data, both prime (340,921sq m) and secondary industrial space (103,760sq m) are at record lows as tenants compete for space.

Knight Frank National Head of Industrial Logistics James Templeton said ongoing strong tenant demand was being met with constrained supply, which had led to increased competition.

“Secondary vacancy is now particularly low as tenants are grabbing immediately available options, with less of a concern regarding grade as long as it is functional,” he said.

“Prime vacancy is also seriously low, however this grade is being somewhat replenished as speculative developments start construction.

“Indeed speculative space accounts for more than two-thirds of the current vacancy – with almost 194,500sq m of this still under construction and not available for imminent occupation.

“As existing options have been absorbed speculative developments have taken a greater weighting in available space.

“This has also supported further prime rental growth with speculative developments needing to set rents at a level which makes the project feasible – at times a further step upward for the market.

“To date these rents have been accepted and embraced by tenants and thus rental growth has remained accelerated.”

Looking ahead, the gradual easing of material cost and supply chain pressures should aid the Eastern Seaboard supply pipeline, allowing it to reach a record of circa 2.5 million square metres in 2023, said Mr Templeton.

“However, 43 per cent of the pipeline is already pre-committed and 10 per cent is owner occupied, so it is unlikely that we will see a significant amount of speculative space entering the market and alleviating the current widespread undersupply,” he said.

The Knight Frank research found Brisbane has a substantial development pipeline, with 843,573sq m forecast to be delivered in 2023, compared to its long-term average of 357,940sq m.

In Sydney new developments are anticipated to reach 807,641sqm, while Melbourne will deliver approximately 845,231sq m.

Related Reading:

New industrial development south of Brisbane gets the go ahead - Knight Frank & JLL

Industrial portfolio Bendigo for sale via Expressions of Interest campaign run by Knight Frank

Important Information:

Contact details:

James Templeton

Knight Frank - National Head of Industrial Logistics

0411 525 217

Email

11406

11142

James Templeton

Jennelle Wilson

Knight Frank, Partner, Research & Consulting, QLD

+61 407 632 064